Contributed by:

Please go through all the slides about training in compliance, AML, fraud prevention, sanctions, KYC, CDD, corporate governance, and cyber security.

1.

EXOTIX ADVISORY LTD -

ANNUAL TRAINING 2022

Compliance, AML and

MAY 2022

2.

01 Exotix Advisory in the DIFC

02 DFSA GEN and COB rules

03 DFSA AML rules

04 Cybersecurity

2

3.

Exotix Advisory in the DIFC

4.

4

Three Key Bodies in the DIFC

1. DIFC Authority

• Oversees strategic development, operational management and planning of the DIFC.

• Oversees development and administration of laws and regulations which apply in the

DIFC (other than those related to the provision of financial services).

2. Dubai Financial Services Authority (DFSA)

• Independent regulator of all financial services conducted in or from the DIFC.

• Authorises, supervises and monitors all financial services firms in the DIFC to ensure

they comply with applicable laws and rules.

• Enforce sanctions in the event of non-compliance.

3. DIFC Courts

• An independent legal system which follows an English common law framework to

deliver international standards of legal procedure and dispute resolution.

• A forum for all civil and commercial DIFC disputes.

5.

5

Dubai Financial Services Authority

• Administers the Regulatory Law, the legislative framework of the regulatory regime. This

Law:

o established the constitution of the DFSA and enabled the creation of the regulatory

framework in which all regulated firms operate; and

o gives the DFSA the power to enforce the Law and the Rules that apply to all regulated

participants within the DIFC.

• Strives to detect and prevent money laundering activities within the DIFC, and also works

closely with the UAE Central Bank in this vital area.

• Follows a principles-based approach to regulation.

• Using these principles as a guide, the DFSA expects all firms to implement their own risk-

based approach to operating within the regulatory regime.

6.

6

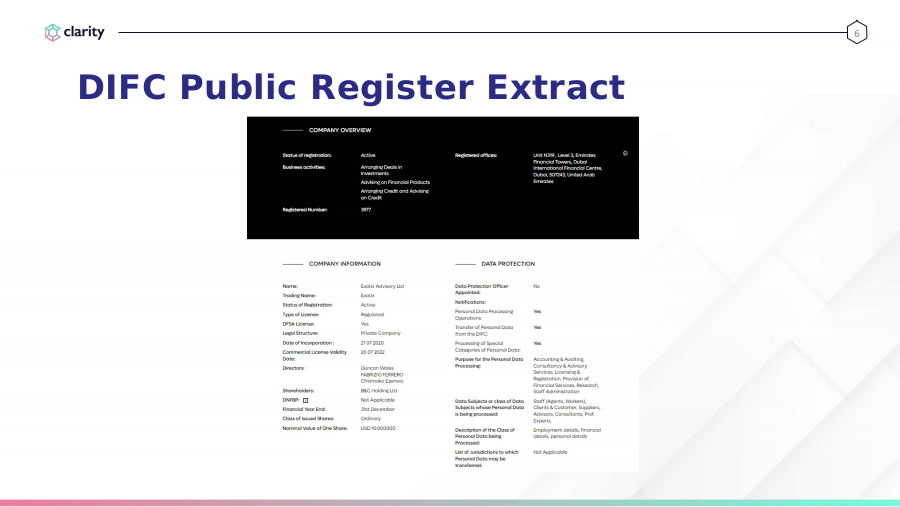

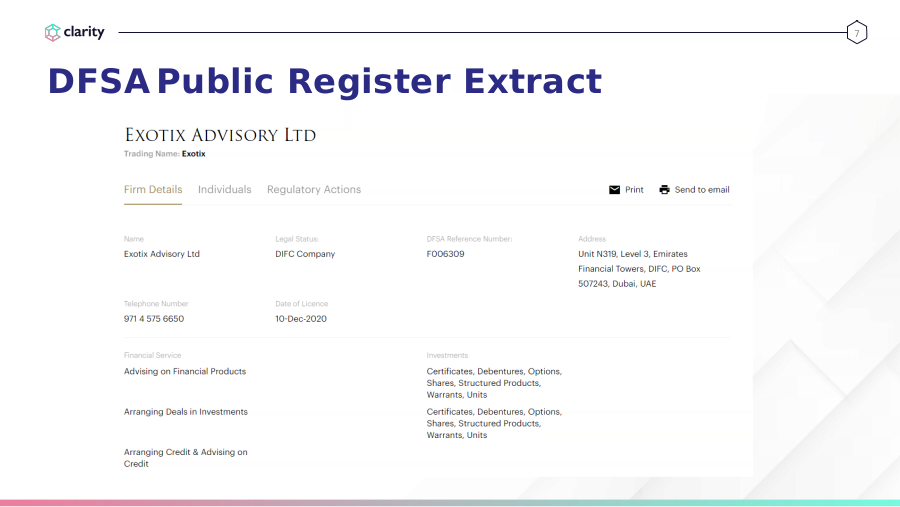

DIFC Public Register Extract

7.

7

DFSA Public Register Extract

8.

8

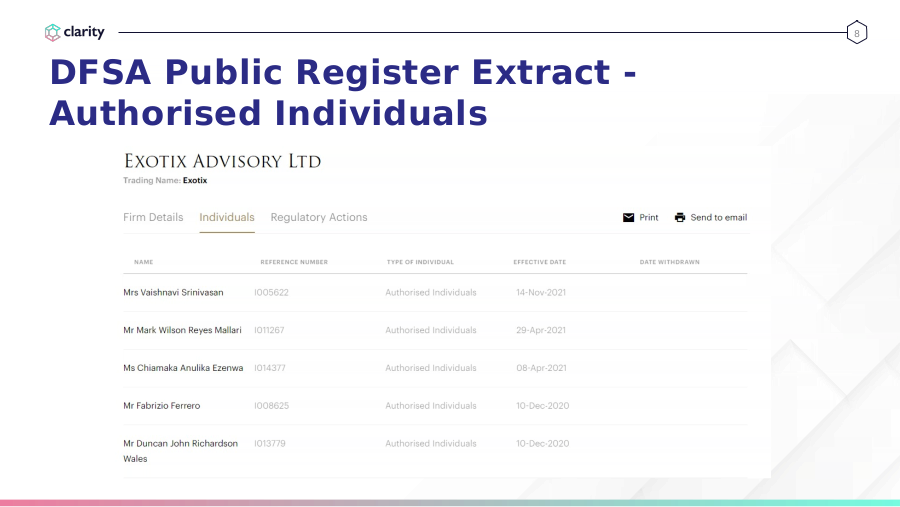

DFSA Public Register Extract -

Authorised Individuals

9.

9

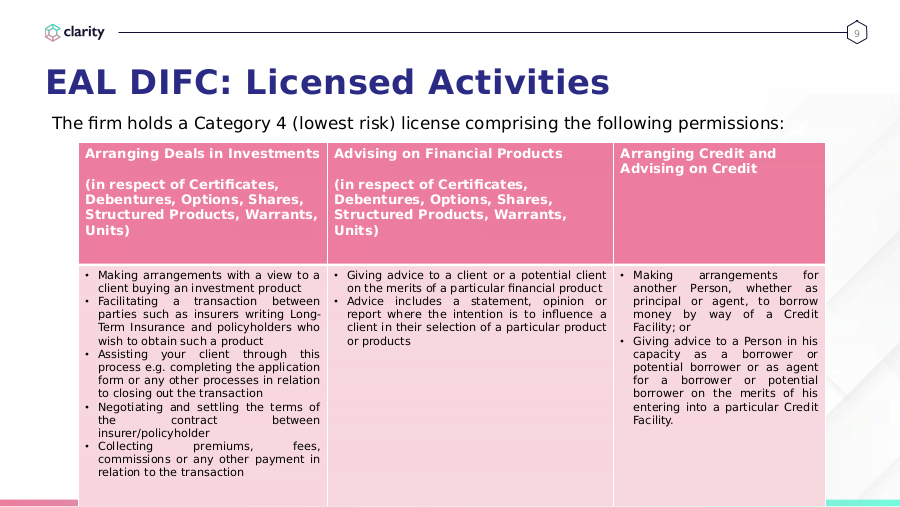

EAL DIFC: Licensed Activities

The firm holds a Category 4 (lowest risk) license comprising the following permissions:

Arranging Deals in Investments Advising on Financial Products Arranging Credit and

Advising on Credit

(in respect of Certificates, (in respect of Certificates,

Debentures, Options, Shares, Debentures, Options, Shares,

Structured Products, Warrants, Structured Products, Warrants,

Units) Units)

• Making arrangements with a view to a • Giving advice to a client or a potential client • Making arrangements for

client buying an investment product on the merits of a particular financial product another Person, whether as

• Facilitating a transaction between • Advice includes a statement, opinion or principal or agent, to borrow

parties such as insurers writing Long- report where the intention is to influence a money by way of a Credit

Term Insurance and policyholders who client in their selection of a particular product Facility; or

wish to obtain such a product or products • Giving advice to a Person in his

• Assisting your client through this capacity as a borrower or

process e.g. completing the application potential borrower or as agent

form or any other processes in relation for a borrower or potential

to closing out the transaction borrower on the merits of his

• Negotiating and settling the terms of entering into a particular Credit

the contract between Facility.

insurer/policyholder

• Collecting premiums, fees,

commissions or any other payment in

relation to the transaction

10.

10

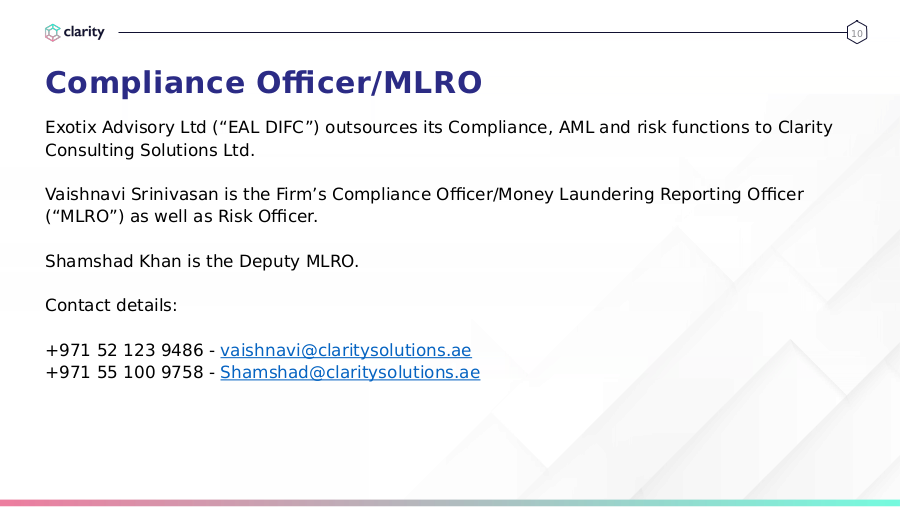

Compliance Officer/MLRO

Exotix Advisory Ltd (“EAL DIFC”) outsources its Compliance, AML and risk functions to Clarity

Consulting Solutions Ltd.

Vaishnavi Srinivasan is the Firm’s Compliance Officer/Money Laundering Reporting Officer

(“MLRO”) as well as Risk Officer.

Shamshad Khan is the Deputy MLRO.

Contact details:

+971 52 123 9486 - [email protected]

+971 55 100 9758 - [email protected]

11.

11

DFSA Principles

• 12 principles for Authorised Firms

o Applicable to activities carried on by the firm from an establishment maintained in the

DIFC

• 6 principles for Authorised Individuals

o Apply in respect of every Licensed Function (like Licensed Director, Senior Manager,

etc.) held by the individual

• Principles have the status of Rules

o Statement of fundamental regulatory requirements

o Rules are built on these fundamental principles

o Apply along with other DFSA Rules

o Also apply in situations that may not be covered by a specific Rule

• Breaching a Principle for Authorised Firms makes the firm liable to disciplinary action, and

may indicate that it is no longer fit and proper to carry on a Financial Service or to hold a

Licence

• Breaching a Principle for Authorised Individuals makes the individual liable to disciplinary

action and may indicate that he is no longer fit and proper to perform a Licensed Function

12.

12

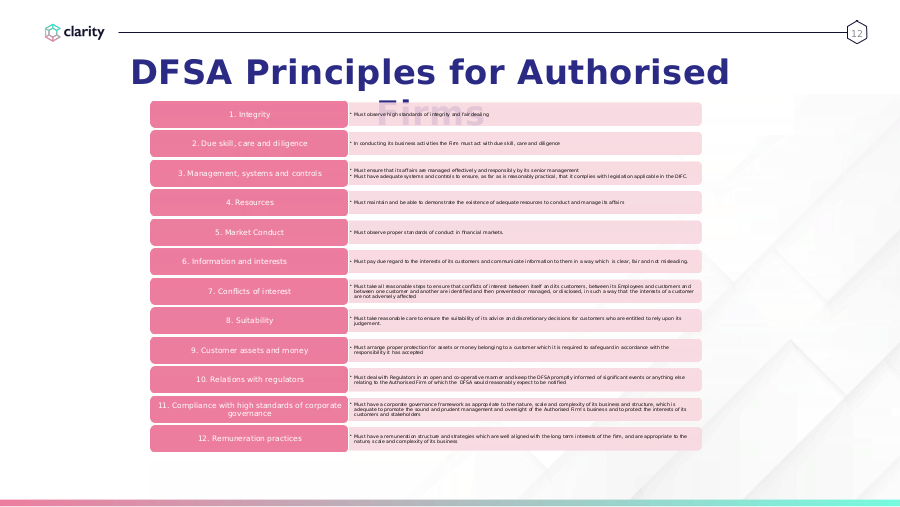

DFSA Principles for Authorised

Firms 1. Integrity • Must observe high standards of integrity and fair dealing

2. Due skill, care and diligence • In conducting its business activities the Firm must act with due skill, care and diligence

• Must ensure that its affairs are managed effectively and responsibly by its senior management

3. Management, systems and controls • Must have adequate systems and controls to ensure, as far as is reasonably practical, that it complies with legislation applicable in the DIFC.

4. Resources • Must maintain and be able to demonstrate the existence of adequate resources to conduct and manage its affairs

5. Market Conduct • Must observe proper standards of conduct in financial markets.

6. Information and interests • Must pay due regard to the interests of its customers and communicate information to them in a way which is clear, fair and not misleading.

• Must take all reasonable steps to ensure that conflicts of interest between itself and its customers, between its Employees and customers and

7. Conflicts of interest between one customer and another are identified and then prevented or managed, or disclosed, in such a way that the interests of a customer

are not adversely affected

• Must take reasonable care to ensure the suitability of its advice and discretionary decisions for customers who are entitled to rely upon its

8. Suitability judgement.

• Must arrange proper protection for assets or money belonging to a customer which it is required to safeguard in accordance with the

9. Customer assets and money responsibility it has accepted

• Must deal with Regulators in an open and co-operative manner and keep the DFSA promptly informed of significant events or anything else

10. Relations with regulators relating to the Authorised Firm of which the DFSA would reasonably expect to be notified

11. Compliance with high standards of corporate • Must have a corporate governance framework as appropriate to the nature, scale and complexity of its business and structure, which is

adequate to promote the sound and prudent management and oversight of the Authorised Firm’s business and to protect the interests of its

governance customers and stakeholders

• Must have a remuneration structure and strategies which are well aligned with the long term interests of the firm, and are appropriate to the

12. Remuneration practices nature, scale and complexity of its business

13.

13

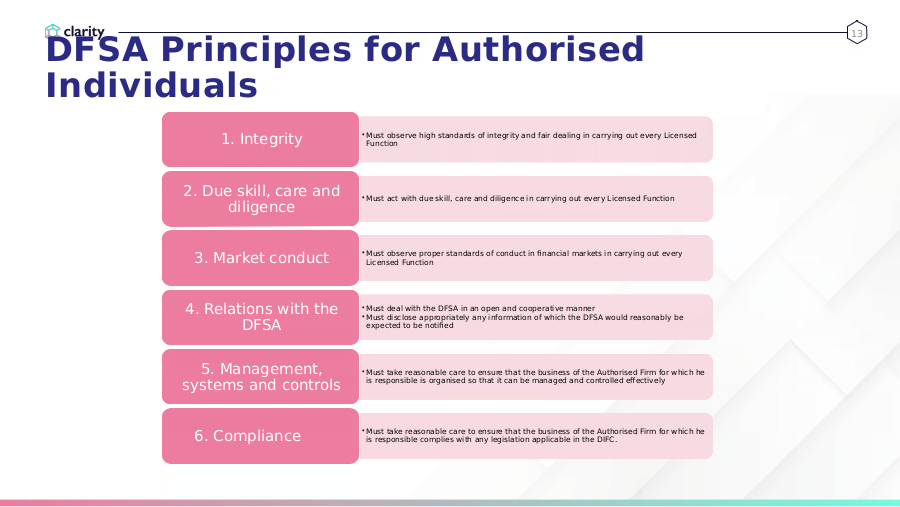

DFSA Principles for Authorised

• Must observe high standards of integrity and fair dealing in carrying out every Licensed

1. Integrity Function

2. Due skill, care and • Must act with due skill, care and diligence in carrying out every Licensed Function

diligence

• Must observe proper standards of conduct in financial markets in carrying out every

3. Market conduct Licensed Function

4. Relations with the • Must deal with the DFSA in an open and cooperative manner

• Must disclose appropriately any information of which the DFSA would reasonably be

DFSA expected to be notified

5. Management, • Must take reasonable care to ensure that the business of the Authorised Firm for which he

systems and controls is responsible is organised so that it can be managed and controlled effectively

• Must take reasonable care to ensure that the business of the Authorised Firm for which he

6. Compliance is responsible complies with any legislation applicable in the DIFC.

14.

DFSA GEN and COB rules

15.

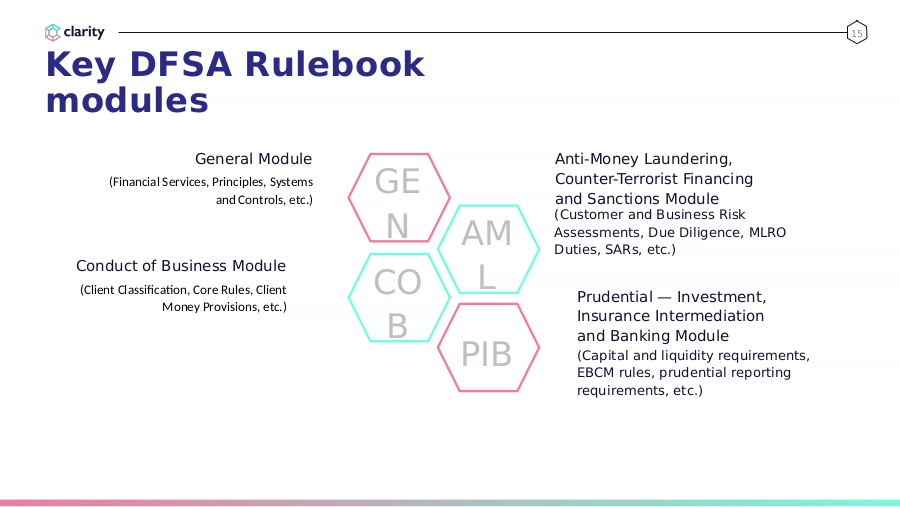

15

Key DFSA Rulebook

General Module Anti-Money Laundering,

(Financial Services, Principles, Systems

and Controls, etc.)

GE Counter-Terrorist Financing

and Sanctions Module

N

(Customer and Business Risk

AM Assessments, Due Diligence, MLRO

Duties, SARs, etc.)

Conduct of Business Module

(Client Classification, Core Rules, Client CO L Prudential — Investment,

Money Provisions, etc.)

B Insurance Intermediation

and Banking Module

PIB (Capital and liquidity requirements,

EBCM rules, prudential reporting

requirements, etc.)

16.

16

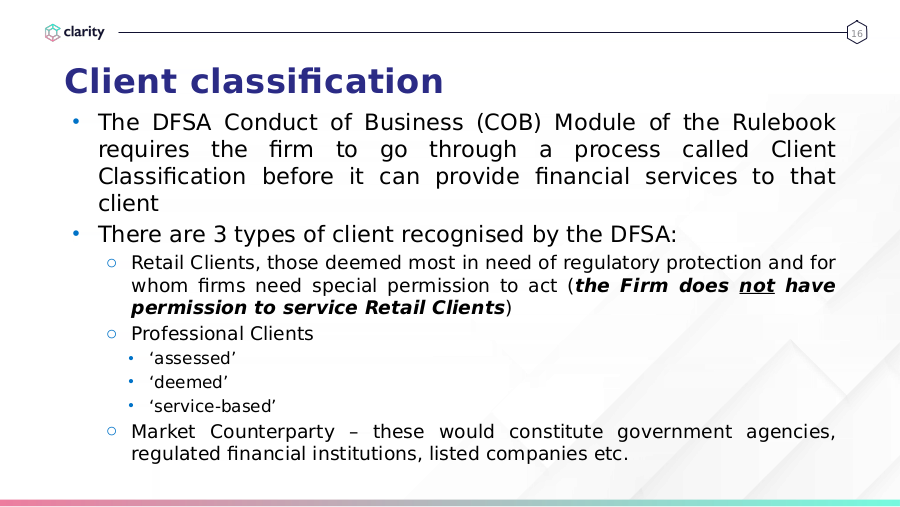

Client classification

• The DFSA Conduct of Business (COB) Module of the Rulebook

requires the firm to go through a process called Client

Classification before it can provide financial services to that

client

• There are 3 types of client recognised by the DFSA:

o Retail Clients, those deemed most in need of regulatory protection and for

whom firms need special permission to act (the Firm does not have

permission to service Retail Clients)

o Professional Clients

• ‘assessed’

• ‘deemed’

• ‘service-based’

o Market Counterparty – these would constitute government agencies,

regulated financial institutions, listed companies etc.

17.

17

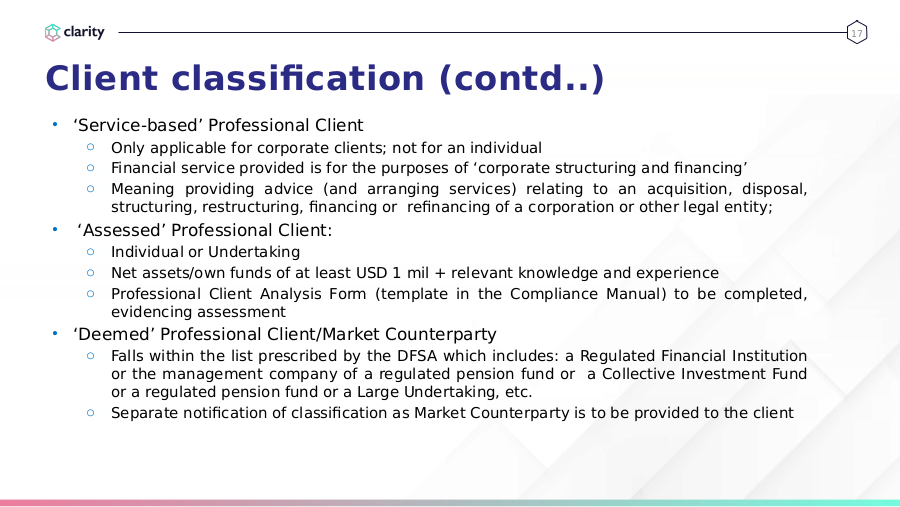

Client classification (contd..)

• ‘Service-based’ Professional Client

o Only applicable for corporate clients; not for an individual

o Financial service provided is for the purposes of ‘corporate structuring and financing’

o Meaning providing advice (and arranging services) relating to an acquisition, disposal,

structuring, restructuring, financing or refinancing of a corporation or other legal entity;

• ‘Assessed’ Professional Client:

o Individual or Undertaking

o Net assets/own funds of at least USD 1 mil + relevant knowledge and experience

o Professional Client Analysis Form (template in the Compliance Manual) to be completed,

evidencing assessment

• ‘Deemed’ Professional Client/Market Counterparty

o Falls within the list prescribed by the DFSA which includes: a Regulated Financial Institution

or the management company of a regulated pension fund or a Collective Investment Fund

or a regulated pension fund or a Large Undertaking, etc.

o Separate notification of classification as Market Counterparty is to be provided to the client

18.

18

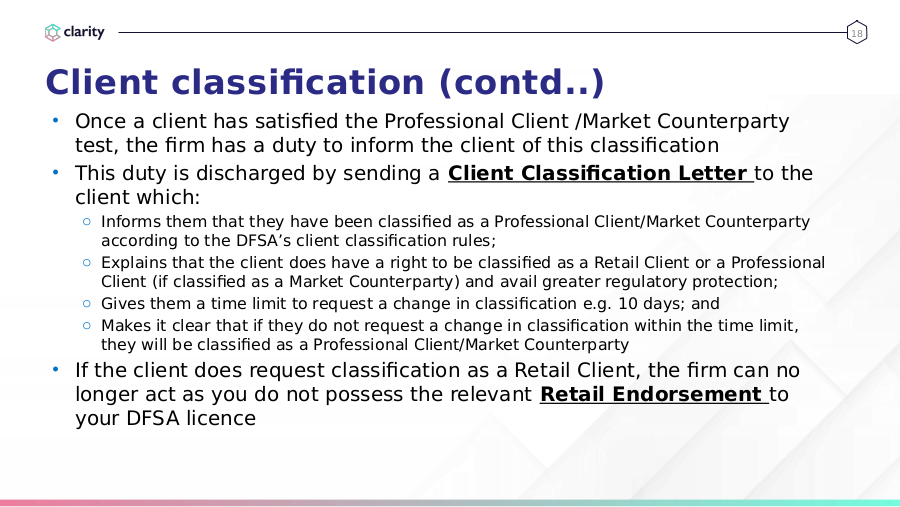

Client classification (contd..)

• Once a client has satisfied the Professional Client /Market Counterparty

test, the firm has a duty to inform the client of this classification

• This duty is discharged by sending a Client Classification Letter to the

client which:

o Informs them that they have been classified as a Professional Client/Market Counterparty

according to the DFSA’s client classification rules;

o Explains that the client does have a right to be classified as a Retail Client or a Professional

Client (if classified as a Market Counterparty) and avail greater regulatory protection;

o Gives them a time limit to request a change in classification e.g. 10 days; and

o Makes it clear that if they do not request a change in classification within the time limit,

they will be classified as a Professional Client/Market Counterparty

• If the client does request classification as a Retail Client, the firm can no

longer act as you do not possess the relevant Retail Endorsement to

your DFSA licence

19.

19

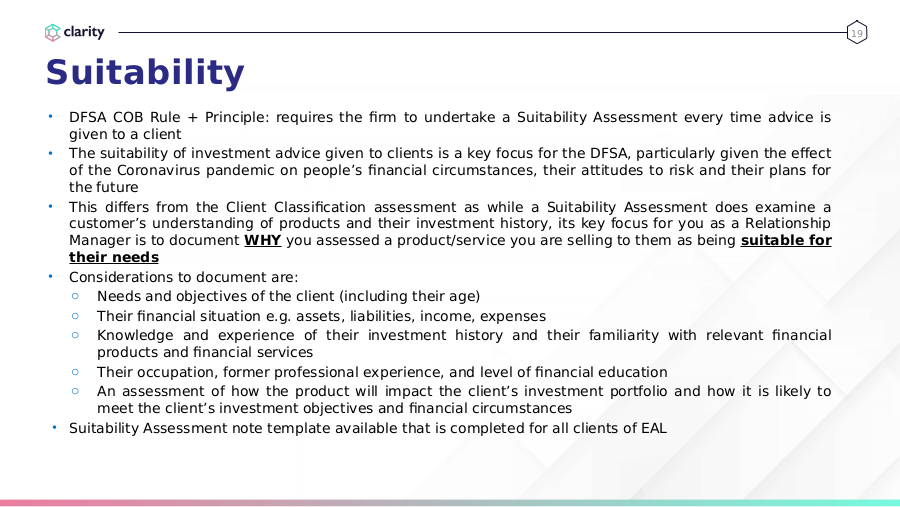

• DFSA COB Rule + Principle: requires the firm to undertake a Suitability Assessment every time advice is

given to a client

• The suitability of investment advice given to clients is a key focus for the DFSA, particularly given the effect

of the Coronavirus pandemic on people’s financial circumstances, their attitudes to risk and their plans for

the future

• This differs from the Client Classification assessment as while a Suitability Assessment does examine a

customer’s understanding of products and their investment history, its key focus for you as a Relationship

Manager is to document WHY you assessed a product/service you are selling to them as being suitable for

their needs

• Considerations to document are:

o Needs and objectives of the client (including their age)

o Their financial situation e.g. assets, liabilities, income, expenses

o Knowledge and experience of their investment history and their familiarity with relevant financial

products and financial services

o Their occupation, former professional experience, and level of financial education

o An assessment of how the product will impact the client’s investment portfolio and how it is likely to

meet the client’s investment objectives and financial circumstances

• Suitability Assessment note template available that is completed for all clients of EAL

20.

20

Marketing Material/Disclosure of Regulatory

• The Firm must ensure that marketing material:

o Is clear, fair and not misleading;

o does not contain information about a specific proposal (generic information about the platform is fine);

o Includes the Firm’s name and regulatory status

• If directed only at Professional Clients/Market Counterparties, is not sent or directed to any person who appears on

reasonable grounds not to be a Professional Client/Market Counterparty and contains a clear statement that only a

person meeting the criteria for Professional Client/Market Counterparty should act upon it.

• All new materials must be approved by Compliance prior to use.

• Every key business document which is in connection with the Firm carrying on a financial service in or from the

DIFC must include one of the following disclosures:

o ‘Regulated by the Dubai Financial Services Authority’

o ‘Regulated by the DFSA’

• Key business documents include:

o Email signatures

o Letterheads

o Terms of business

o Written promotional materials

o Business Cards

o Websites

21.

21

Conflicts of Interest

• Could arise between firm and clients, employees and clients, or between clients

• The firm must have systems and controls in place identify and prevent/manage conflicts

(DFSA rule and principle)

• These typically consist of implementing Chinese Walls where relevant; disclosing conflicts to

the client in writing, requiring employees to disregard any conflict of interest when advising a

client, etc.

• Where a conflict cannot be prevented/managed, the firm must decline to act for that Client

• Systems and procedures include the following measures for preventing and managing

conflicts:

o Conflicts of Interests Policy in the Compliance Manual

o Policy to disclose personal account transactions

o Policy to disclose gifts and entertainments

o Policy to disclose external business interests

o Maintaining Insider List

22.

22

Conflicts of Interest (contd..)

• Gifts and hospitality

o Employees are not allowed to accept gifts, entertainment or any other inducement from any person

which might benefit one customer at the expense of another

o Compliance Officer to be consulted before providing or receiving any sort of inducement to or from

another

o Gifts may be received/given only when they are consistent with business practice, are of reasonable

value and do not violate any law/ethical standards

o Cash/cash equivalent gifts are prohibited at all times

• Outside business activities

o Could be other employment/directorships/political activity/shareholding, etc.

o Employees are required to disclose external business interests upon joining the firm

o For any new activities contemplated during employment with the firm, prior approval needs to be

sought using form in the Compliance Manual

• Insider list

o Firm maintains insider lists for projects where customers or companies involved have publicly listed

financial instruments to ensure the people with knowledge of the situations are clearly identified

23.

23

Conflicts of Interest (contd..)

• Personal account dealing

o All trade pre-approval must be sought (in writing) from the SEO (or the Compliance

Officer)

o Once pre-approval is granted, employees have up to 5 business days to execute your

trade

o PA transactions over which you have no discretion should be reported to the Compliance

Officer as soon as possible

o This reporting requirement extends to any trading in bonds, equities, swaps, warrants,

contracts for difference and spread bets (but not non‐financial spread bets such as those

on sports events)

o The restrictions also apply to any transaction undertaken by members of your family

(e.g., your spouse, children under 18 and those with close links to the employee)

o Copies of contract notes (similar) should be provided to the Compliance Officer post-trade

• Starting July 2022, EAL will be obtaining declarations from employees twice a year in

relation to matters such as personal account transactions, outside business interests,

etc.

24.

24

Complaints handling

• A customer complaint is any expression of dissatisfaction about

any aspect of the Firm’s business or about the activities of any

employee:

o Verbal or written

o Justified or not

o From a client/prospect/service provider

• All complaints should be investigated and resolved fairly,

consistently and promptly

• Where systemic problems are identified, systems and controls

should be reviewed and enhanced to ensure there is no repetition

• Appropriate records (including Complaints Notification Form)

should be maintained.

25.

25

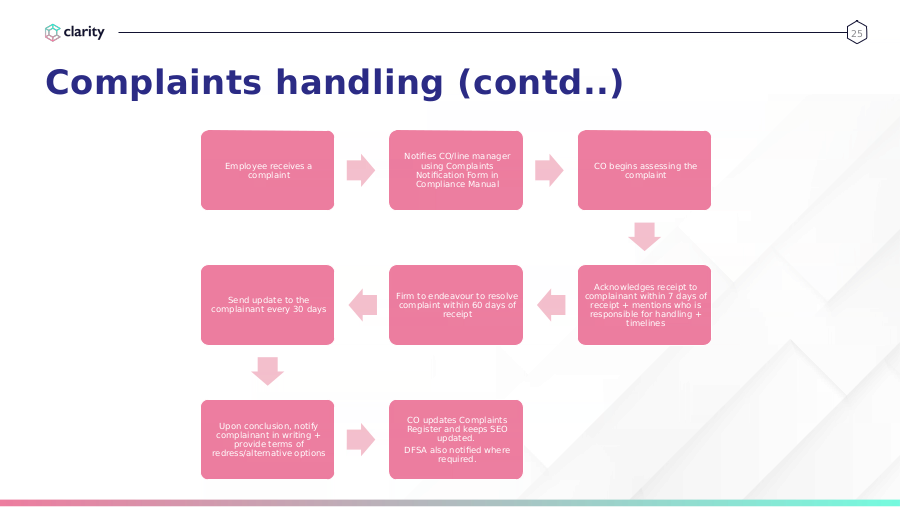

Complaints handling (contd..)

Notifies CO/line manager

Employee receives a using Complaints CO begins assessing the

complaint Notification Form in complaint

Compliance Manual

Acknowledges receipt to

Firm to endeavour to resolve complainant within 7 days of

Send update to the

complaint within 60 days of receipt + mentions who is

complainant every 30 days

receipt responsible for handling +

timelines

CO updates Complaints

Upon conclusion, notify Register and keeps SEO

complainant in writing + updated.

provide terms of

redress/alternative options DFSA also notified where

required.

26.

26

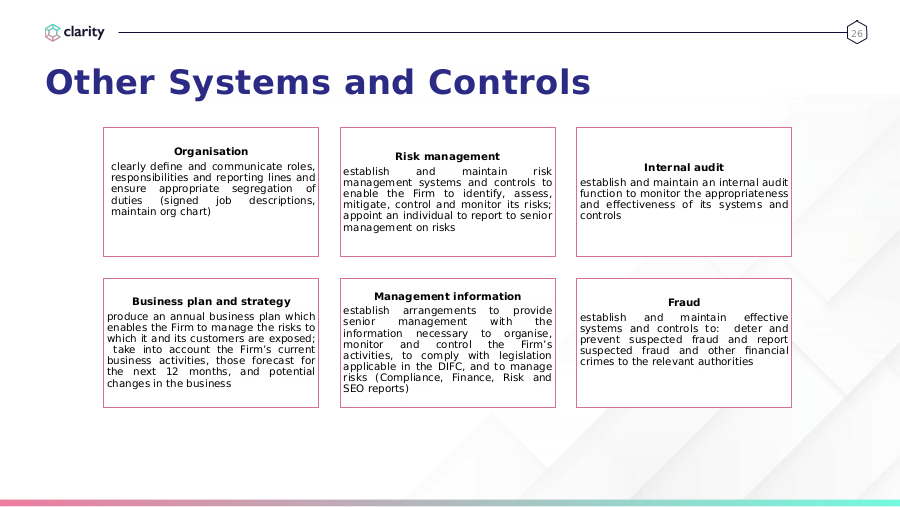

Other Systems and Controls

Organisation Risk management

clearly define and communicate roles, establish and maintain risk Internal audit

responsibilities and reporting lines and management systems and controls to establish and maintain an internal audit

ensure appropriate segregation of enable the Firm to identify, assess, function to monitor the appropriateness

duties (signed job descriptions, mitigate, control and monitor its risks; and effectiveness of its systems and

maintain org chart) appoint an individual to report to senior controls

management on risks

Management information

Business plan and strategy Fraud

establish arrangements to provide

produce an annual business plan which establish and maintain effective

senior management with the

enables the Firm to manage the risks to systems and controls to: deter and

information necessary to organise,

which it and its customers are exposed; prevent suspected fraud and report

monitor and control the Firm’s

take into account the Firm’s current suspected fraud and other financial

activities, to comply with legislation

business activities, those forecast for crimes to the relevant authorities

applicable in the DIFC, and to manage

the next 12 months, and potential

risks (Compliance, Finance, Risk and

changes in the business

SEO reports)

27.

27

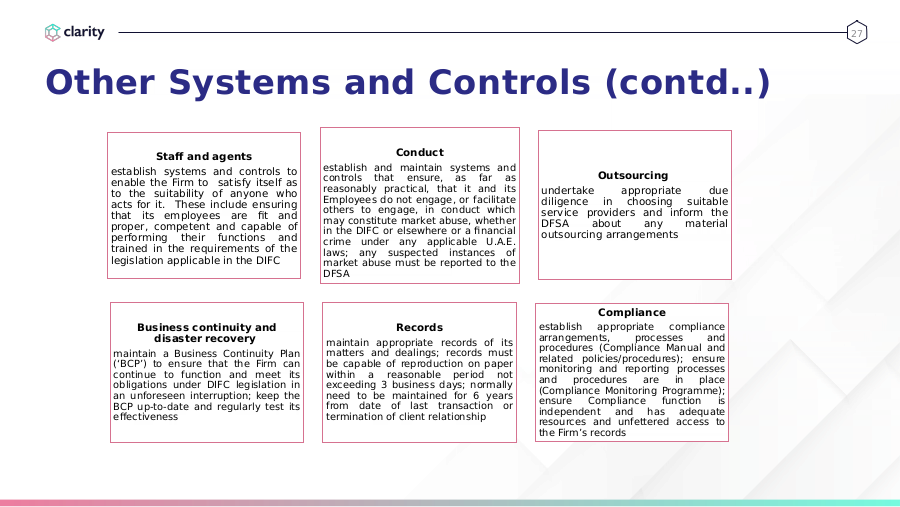

Other Systems and Controls (contd..)

Staff and agents Conduct

establish systems and controls to establish and maintain systems and

controls that ensure, as far as Outsourcing

enable the Firm to satisfy itself as

reasonably practical, that it and its undertake appropriate due

to the suitability of anyone who

Employees do not engage, or facilitate diligence in choosing suitable

acts for it. These include ensuring

others to engage, in conduct which service providers and inform the

that its employees are fit and may constitute market abuse, whether

proper, competent and capable of DFSA about any material

in the DIFC or elsewhere or a financial outsourcing arrangements

performing their functions and crime under any applicable U.A.E.

trained in the requirements of the laws; any suspected instances of

legislation applicable in the DIFC market abuse must be reported to the

DFSA

Compliance

Business continuity and Records establish appropriate compliance

disaster recovery arrangements, processes and

maintain appropriate records of its

procedures (Compliance Manual and

maintain a Business Continuity Plan matters and dealings; records must

related policies/procedures); ensure

(‘BCP’) to ensure that the Firm can be capable of reproduction on paper

monitoring and reporting processes

continue to function and meet its within a reasonable period not

and procedures are in place

obligations under DIFC legislation in exceeding 3 business days; normally

(Compliance Monitoring Programme);

an unforeseen interruption; keep the need to be maintained for 6 years

ensure Compliance function is

BCP up-to-date and regularly test its from date of last transaction or

independent and has adequate

effectiveness termination of client relationship

resources and unfettered access to

the Firm’s records

28.

28

• DFSA introduced new rules that came into effect on 07 April, 2022

• Compliance Manual will be updated in May 2022 to reflect the same

• Procedure described for reporting instances internally within the firm in the first instance

• Employees can also approach the DFSA or other relevant authority directly instead, or

simultaneously, if deemed necessary

• Reports to the DFSA can be sent at [email protected]

• Regulatory Law provides legal protection to a whistleblower who discloses information about

suspected misconduct in good faith under certain circumstances.

o Protection is from liability, dismissal or detriment for making that disclosure

o Does not prevent the Firm from taking action against an employee for other legitimate reasons, such

as if the employee has engaged in misconduct.

• No employee who in good faith reports a violation shall suffer harassment, retaliation or

adverse employment consequence.

30.

30

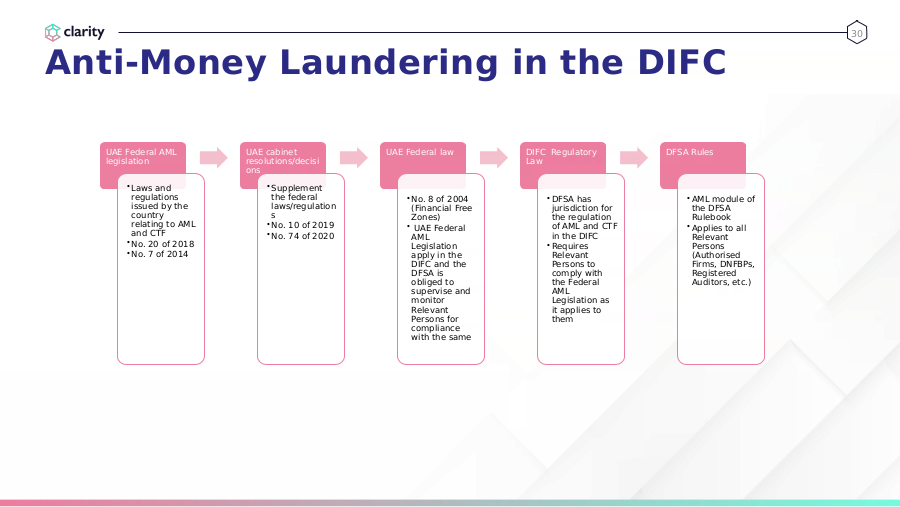

Anti-Money Laundering in the DIFC

UAE Federal AML UAE cabinet UAE Federal law DIFC Regulatory DFSA Rules

legislation resolutions/decisi Law

ons

• Laws and • Supplement

regulations the federal • No. 8 of 2004 • DFSA has • AML module of

issued by the laws/regulation (Financial Free jurisdiction for the DFSA

country s Zones) the regulation Rulebook

relating to AML • No. 10 of 2019 • UAE Federal of AML and CTF • Applies to all

and CTF • No. 74 of 2020 AML in the DIFC Relevant

• No. 20 of 2018 Legislation • Requires Persons

• No. 7 of 2014 apply in the Relevant (Authorised

DIFC and the Persons to Firms, DNFBPs,

DFSA is comply with Registered

obliged to the Federal Auditors, etc.)

supervise and AML

monitor Legislation as

Relevant it applies to

Persons for them

compliance

with the same

31.

31

Definitions of terms

Money Laundering

The process of concealing the origins of funds obtained through some form of illegal activity,

typically through transactions involving foreign banks or legitimate businesses, in order to

make the funds appear legitimate

• Must involve criminal activity which generates proceeds of crime to be laundered

• Must involve some element of transfer or usage of funds with intent either to hide

their criminal origins or to use them for their own ends

• The laundering of money makes it appear legitimate so that those doing the

laundering benefit directly from it by funding their lifestyle e.g. purchasing goods,

making investments etc.

Terrorism Financing

The provision of funds or ongoing financial support to enable individual terrorists or terrorist

groups to carry out unlawful terrorist activity

• Funds used do not have to be proceeds of crime, can have been earned legitimately

• Funds are used to support criminal activity

• The beneficiaries are the terrorists, not those who raise the funds

32.

32

What constitutes “Criminal Activity”?

Narcotics

Any other and

related psychotropic

offences in substances

international Kidnapping

agreements to

which UAE is

party

Fraud, breach

of trust and

related

Piracy

offences

Criminal

Activity

Embezzle-

Terrorism

ment

Violation of

Bribery and

Corruption

environ-

Illicit dealing mental law

in firearms

and

ammunition

33.

33

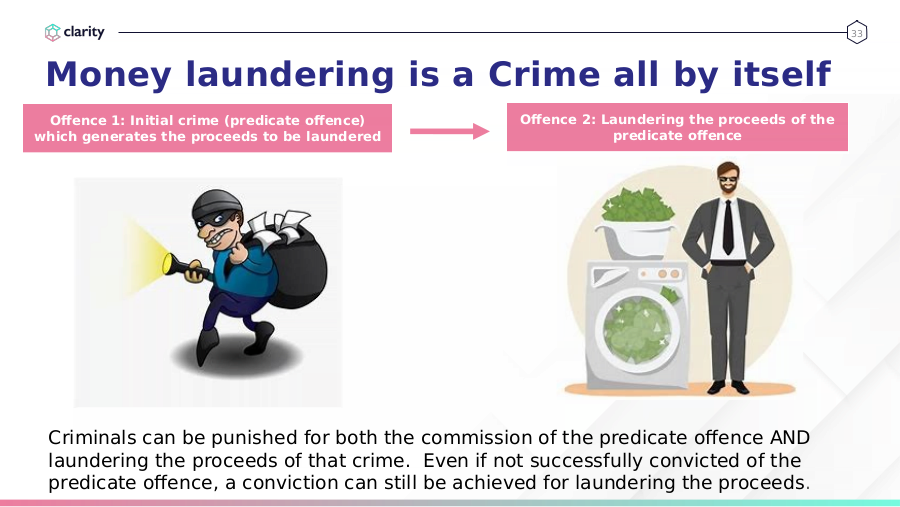

Money laundering is a Crime all by itself

Offence 1: Initial crime (predicate offence) Offence 2: Laundering the proceeds of the

which generates the proceeds to be laundered predicate offence

Criminals can be punished for both the commission of the predicate offence AND

laundering the proceeds of that crime. Even if not successfully convicted of the

predicate offence, a conviction can still be achieved for laundering the proceeds.

34.

34

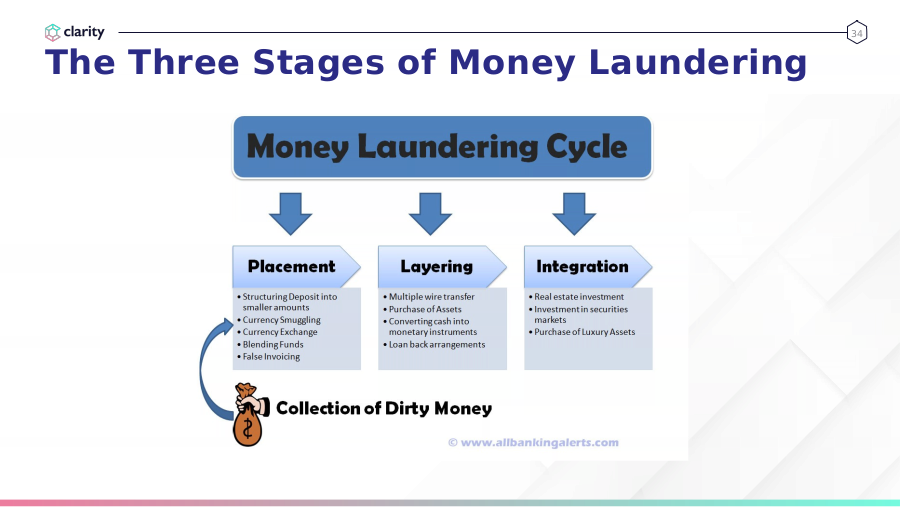

The Three Stages of Money Laundering

35.

35

Preventative AML Measures

Who is responsible? Everyone!

Each member of Senior Management (SEO, Finance Officer,

CO/MLRO) is responsible for delivering compliance with the

relevant AML requirements by the whole office

• All staff are responsible for complying with policies and procedures,

attending training, and reporting suspicious activities (first line of

defence)

• The MLRO is responsible for the implementation of the AML

framework and day to day oversight of compliance with AML Rules

(second line of defence)

36.

36

DFSA – Risk-Based Approach

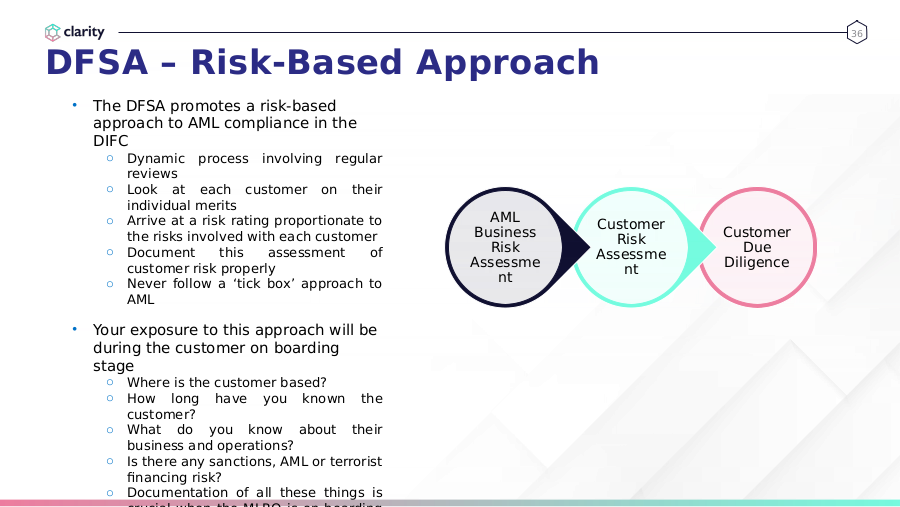

• The DFSA promotes a risk-based

approach to AML compliance in the

DIFC

o Dynamic process involving regular

reviews

o Look at each customer on their

individual merits

o Arrive at a risk rating proportionate to AML

Customer

the risks involved with each customer Business Customer

Risk

o Document this assessment of Risk Due

Assessme

customer risk properly Assessme Diligence

nt

o Never follow a ‘tick box’ approach to nt

AML

• Your exposure to this approach will be

during the customer on boarding

stage

o Where is the customer based?

o How long have you known the

customer?

o What do you know about their

business and operations?

o Is there any sanctions, AML or terrorist

financing risk?

o Documentation of all these things is

37.

37

Three Pillars

AML Business Risk Customer Risk Customer Due

Assessment Assessment Diligence

• Low risk • Low risk • Simplified

• Medium • Medium • Standard

risk risk • Enhanced

• High risk • High risk

38.

38

AML Business Risk Assessment

• Annual mandatory assessment of AML risks to your business

• Clearly documented and approved by Senior Management

• The MLRO assesses the AML risks across 7 key areas:

o your clients and their activities;

o the countries in which you do business;

o your products, services and activity profiles;

o your distribution channels and business partners;

o the complexity and volume of business transactions;

o the development of any new products, business practices,

channels and partners; and

o the use of new or developing technologies for both new

and existing products.

• The information gathered then helps the business:

o develop, implement and sustain effective AML policies,

procedures, systems and controls in order to mitigate the

risks identified;

o review the effectiveness of these controls at least annually;

o prioritise the allocation of AML resources; and

o assist in the carrying out of the Customer Risk Assessment.

39.

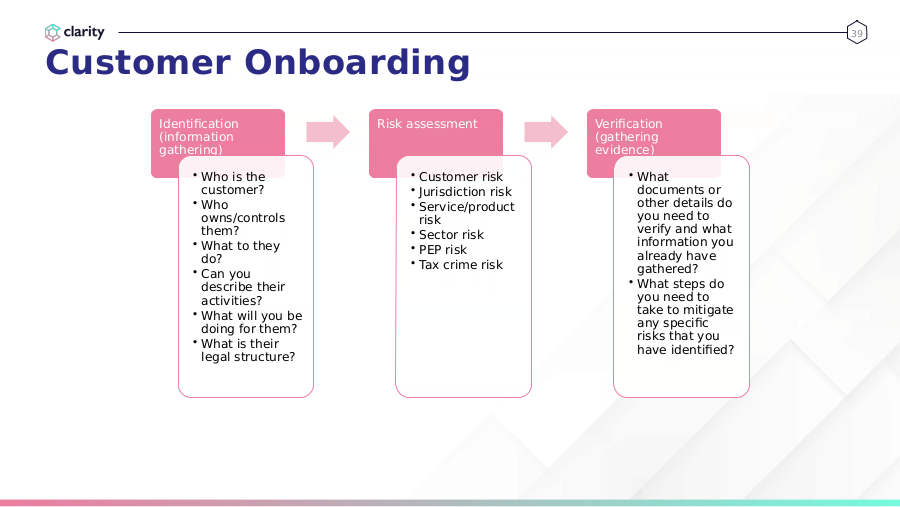

39

Customer Onboarding

Identification Risk assessment Verification

(information (gathering

gathering) evidence)

• Who is the • Customer risk • What

customer? • Jurisdiction risk documents or

• Who • Service/product other details do

owns/controls risk you need to

them? • Sector risk verify and what

• What to they • PEP risk information you

do? already have

• Tax crime risk gathered?

• Can you

describe their • What steps do

activities? you need to

• What will you be take to mitigate

doing for them? any specific

• What is their risks that you

have identified?

legal structure?

40.

40

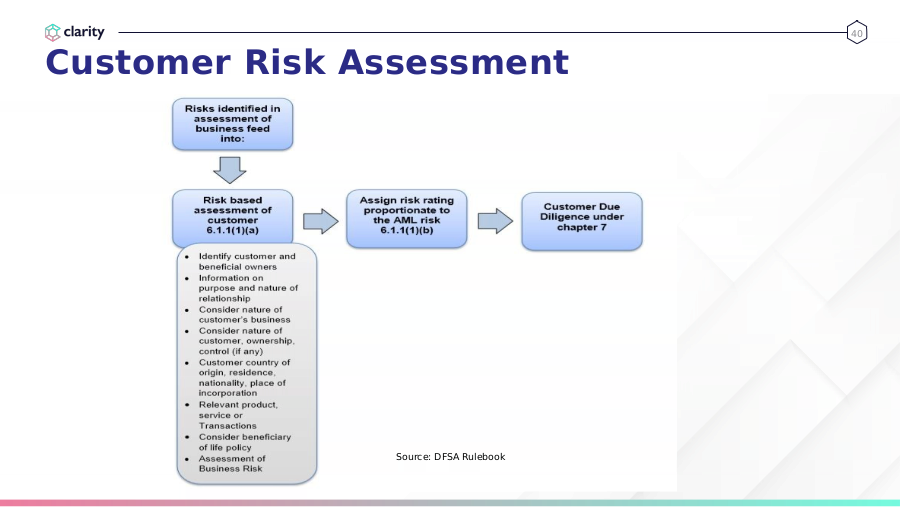

Customer Risk Assessment

Source: DFSA Rulebook

41.

41

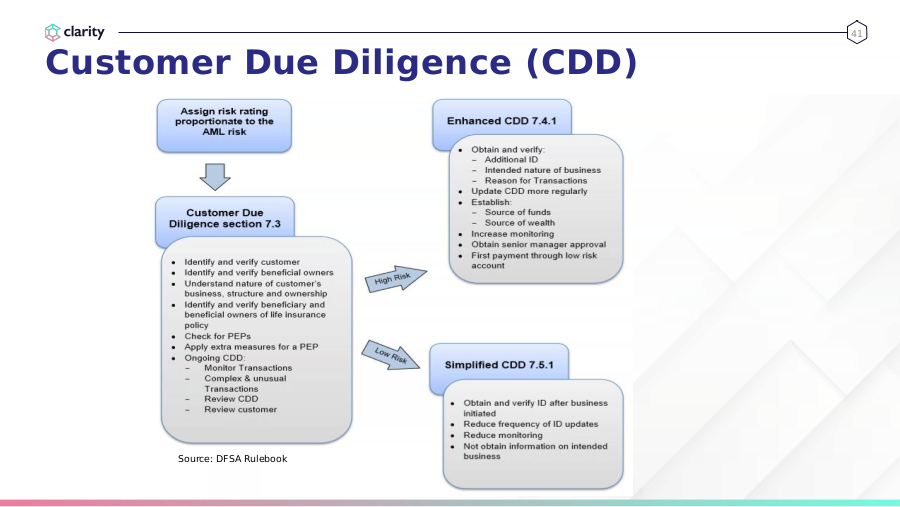

Customer Due Diligence (CDD)

Source: DFSA Rulebook

42.

42

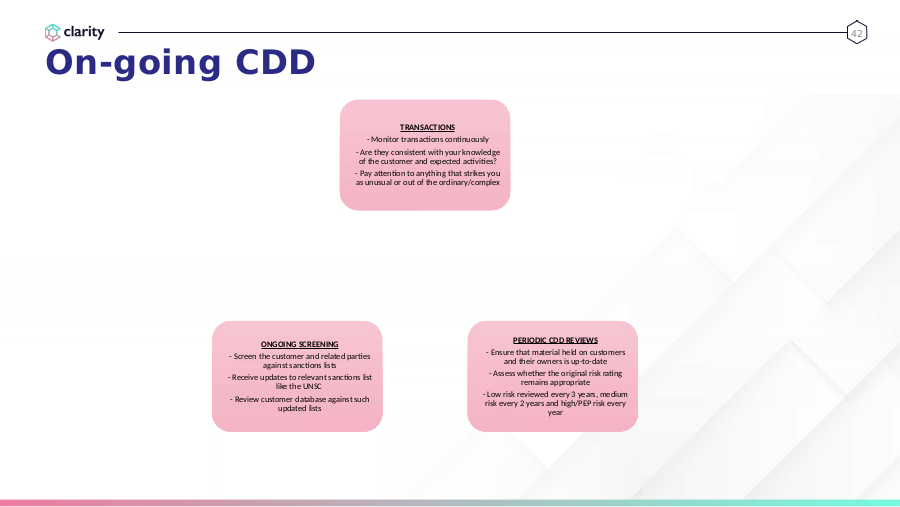

On-going CDD

TRANSACTIONS

- Monitor transactions continuously

- Are they consistent with your knowledge

of the customer and expected activities?

- Pay attention to anything that strikes you

as unusual or out of the ordinary/complex

PERIODIC CDD REVIEWS

ONGOING SCREENING

- Ensure that material held on customers

- Screen the customer and related parties

and their owners is up-to-date

against sanctions lists

- Assess whether the original risk rating

- Receive updates to relevant sanctions list

remains appropriate

like the UNSC

- Low risk reviewed every 3 years, medium

- Review customer database against such

risk every 2 years and high/PEP risk every

updated lists

year

43.

43

Politically Exposed Persons (PEPs)

Definition (DFSA AML glossary):

“A natural person (and includes, where relevant, a

family member or close associate) who is or has been

entrusted with a prominent public function, whether in

the State or elsewhere, including but not limited to, a

head of state or of government, senior politician, senior

government, judicial or military official, ambassador,

senior person in an International Organisation, senior

executive of a state owned corporation, an important

political party official, or a member of senior

management or an individual who has been entrusted

with similar functions such as a director or a deputy

director. This definition does not include middle ranking

or more junior individuals in the above categories.”

44.

44

Politically Exposed Persons (contd..)

• Presence of PEPs does not automatically make a customer high risk. But firm

has to assess whether there is a possibility that individuals holding such

positions have misused their power and influence for personal gain or

advantage.

• Factors to be considered include:

o Position of the PEP

o Domestic or foreign PEP

o Associated jurisdiction risk

o Adverse news relating to the PEP

• DFSA rules require additional action to be taken where PEPs are identified:

o Senior management approval to onboard

o Increased monitoring

o Reasonably establishing source of funds and wealth

45.

45

Sanctions compliance

• The firm must maintain effective systems and controls to make use of relevant

findings, recommendations, guidance, directives, resolutions or sanctions issued

by:

o UN Security Council

o the government of the U.A.E. or any government departments in the U.A.E.;

o the Central Bank of the U.A.E. or the FIU;

o FATF;

o U.A.E. enforcement agencies; and

o the DFSA

• The firm must immediately notify the DFSA when it becomes aware that it is:

o carrying on or about to carry on an activity;

o holding or about to hold money or other assets; or

o undertaking or about to undertake any other business whether or not arising

from or in connection with the above points;

for or on behalf of a person, where such carrying on, holding or undertaking

constitutes or may constitute a contravention of a relevant sanction or resolution

issued by the UN Security Council.

46.

46

Targeted Financial Sanctions (TFS)

• The term ‘targeted sanctions’ means that sanctions are imposed against specific

individuals or groups, or undertakings.

• The term ‘targeted financial sanctions’ (TFS) includes both asset freezing and

prohibitions to prevent funds or other assets from being made available, directly

or indirectly, for the benefit of individuals, entities, groups, or organization who

are sanctioned.

• The freezing measures, including the prohibition of making funds available, apply

to:

o Any individual, group, or entity listed in the Local (UAE) Terrorist List or listed

by the UNSC.

o Any entity, directly or indirectly owned or controlled by an individual or entity

listed under A.

o Any individual or entity acting on behalf of or at the direction of any individual

or Entity listed above.

47.

47

Targeted Financial Sanctions (contd..)

All UAE Financial Institutions including the Firm must:

• Register at the Executive Office website to receive automated email notifications

https://www.uaeiec.gov.ae

• Undertake ongoing and daily checks to the following databases to identify

possible matches with names listed in the Sanctions Lists issued by the UN List or

the UAE Local Terrorist List

• Apply TFS (i.e. freezing measures) immediately and without delay (within 24

hours) if a match with the UN List or the Local Terrorist List is identified

• Immediately notify the DFSA as Supervisory Authority about having applied TFS

• Submit a Funds Freeze Report (FFR) or Partial Name Match Report (PNMR)as

applicable via the goAML portal within 5 business days from taking any freezing

measure and/or attempted transactions. Submissions via the goAML portal are

received by the Executive Office as well as the DFSA.

• Cooperate with the Executive Office and the DFSA in verifying the accuracy of the

submitted information submitted

• Implement the freezing cancellation or lifting decision, when appropriate, without

delay.

48.

48

Suspicious Activity Reports (SARs)

• Whenever any employee, acting in the ordinary course of his employment, either:

o knows;

o suspects; or

o has reasonable grounds for knowing or suspecting;

that a person is engaged in or attempting money laundering or terrorist financing, the employee must promptly

notify the MLRO and provide the MLRO with all relevant details (Internal Suspicious Activity Report).

This is a legal obligation.

• On receipt of an internal SAR, the MLRO will undertake requisite reviews/investigate the matter further and

decide on whether or not a SAR needs to be filed with the UAE’s Financial Intelligence Unit (External Suspicious

Activity Report)

• Filing SARs upon noticing any suspicious activity is a requirement under UAE federal laws as well as DFSA AML

rules.

• In the absence of the MLRO, the firm’s Deputy MLRO will assume the above-mentioned responsibilities.

49.

49

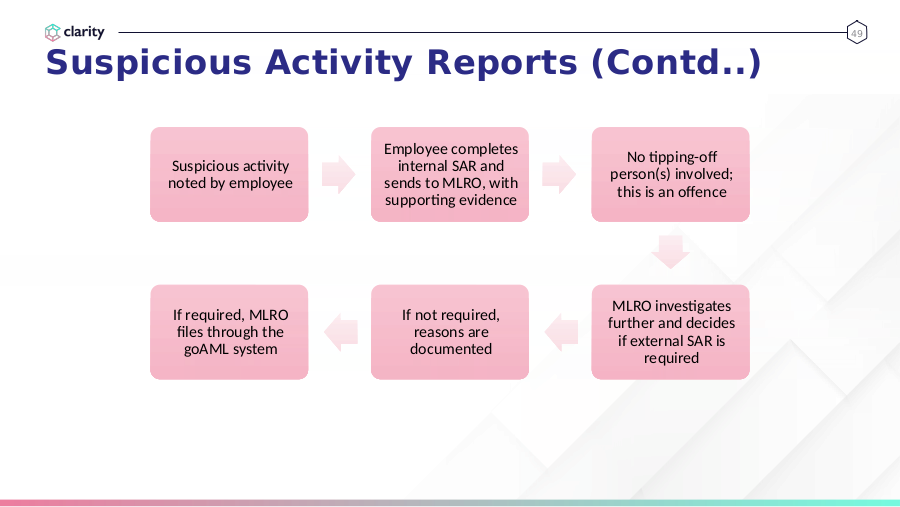

Suspicious Activity Reports (Contd..)

Employee completes

No tipping-off

Suspicious activity internal SAR and

person(s) involved;

noted by employee sends to MLRO, with

this is an offence

supporting evidence

MLRO investigates

If required, MLRO If not required,

further and decides

files through the reasons are

if external SAR is

goAML system documented

required

50.

50

Red Flags

• Customer uses unusual or suspicious

identification documents that cannot be

readily verified;

• Customer is reluctant, when establishing

a new relationship, to provide complete

information;

• Customer’s background differs from that

which would be expected on the basis of

his or her business activities;

• Customer is reluctant to provide

information on controlling parties and

underlying beneficiaries;

• Any other unusual requests outside the

normal pattern expected.

51.

51

DFSA Thematic Review – AML in the

Brokerage sector

• In Nov 2021, the DFSA released findings and observations stemming from its thematic review on

the AML processes applied by brokerage firms specifically.

• Contained findings and observations for firms while undertaking AML Business Risk Assessment and

customer risk assessments/due diligence

• Though the thematic review was in relation to a specific category of firms (i.e. the brokerage

sector), the findings/observations can be implemented by other regulated entities as well.

• EAL DIFC’s latest AML Business Risk Assessment (Apr 2022 version) has considered the DFSA’s

recommendations contained in the above report.

52.

52

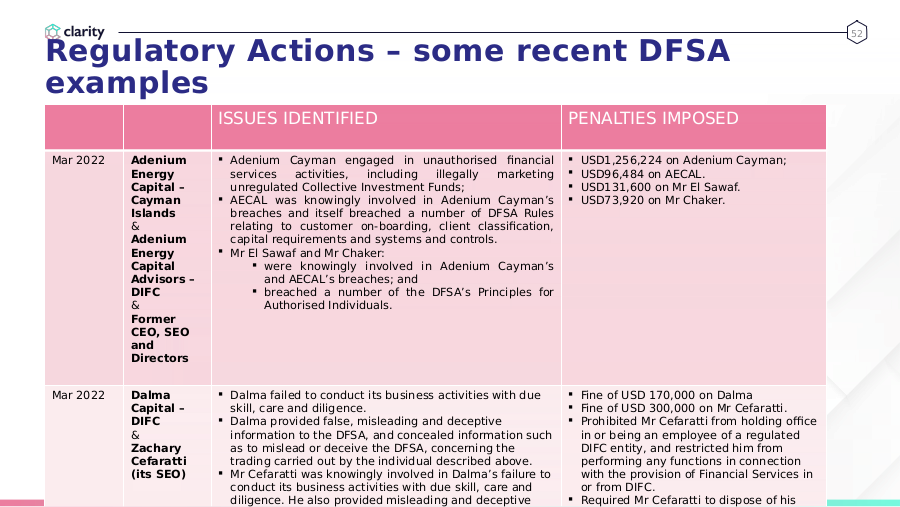

Regulatory Actions – some recent DFSA

ISSUES IDENTIFIED PENALTIES IMPOSED

Mar 2022 Adenium Adenium Cayman engaged in unauthorised financial USD1,256,224 on Adenium Cayman;

Energy services activities, including illegally marketing USD96,484 on AECAL.

Capital – unregulated Collective Investment Funds; USD131,600 on Mr El Sawaf.

Cayman AECAL was knowingly involved in Adenium Cayman’s USD73,920 on Mr Chaker.

Islands breaches and itself breached a number of DFSA Rules

& relating to customer on-boarding, client classification,

Adenium capital requirements and systems and controls.

Energy Mr El Sawaf and Mr Chaker:

Capital were knowingly involved in Adenium Cayman’s

Advisors – and AECAL’s breaches; and

DIFC breached a number of the DFSA’s Principles for

& Authorised Individuals.

Former

CEO, SEO

and

Directors

Mar 2022 Dalma Dalma failed to conduct its business activities with due Fine of USD 170,000 on Dalma

Capital – skill, care and diligence. Fine of USD 300,000 on Mr Cefaratti.

DIFC Dalma provided false, misleading and deceptive Prohibited Mr Cefaratti from holding office

& information to the DFSA, and concealed information such in or being an employee of a regulated

Zachary as to mislead or deceive the DFSA, concerning the DIFC entity, and restricted him from

Cefaratti trading carried out by the individual described above. performing any functions in connection

(its SEO) Mr Cefaratti was knowingly involved in Dalma’s failure to with the provision of Financial Services in

conduct its business activities with due skill, care and or from DIFC.

diligence. He also provided misleading and deceptive Required Mr Cefaratti to dispose of his

53.

53

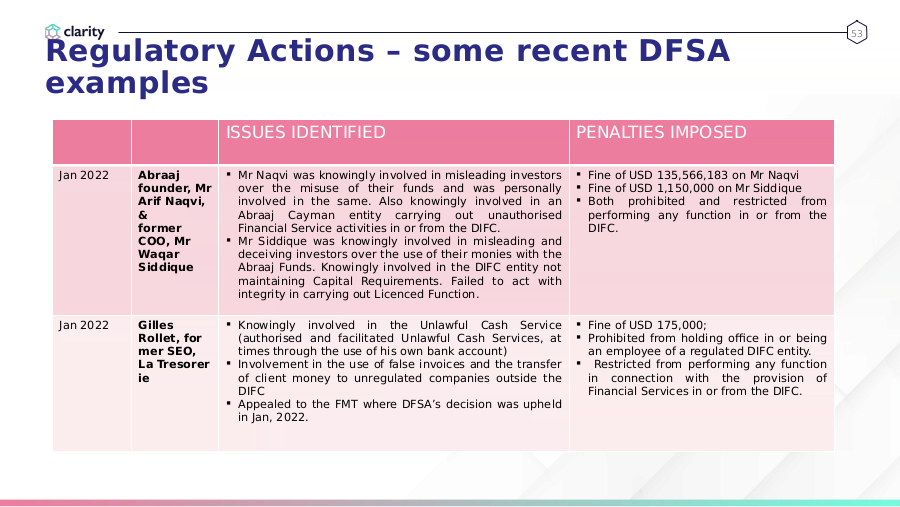

Regulatory Actions – some recent DFSA

ISSUES IDENTIFIED PENALTIES IMPOSED

Jan 2022 Abraaj Mr Naqvi was knowingly involved in misleading investors Fine of USD 135,566,183 on Mr Naqvi

founder, Mr over the misuse of their funds and was personally Fine of USD 1,150,000 on Mr Siddique

Arif Naqvi, involved in the same. Also knowingly involved in an Both prohibited and restricted from

& Abraaj Cayman entity carrying out unauthorised performing any function in or from the

former Financial Service activities in or from the DIFC. DIFC.

COO, Mr Mr Siddique was knowingly involved in misleading and

Waqar deceiving investors over the use of their monies with the

Siddique Abraaj Funds. Knowingly involved in the DIFC entity not

maintaining Capital Requirements. Failed to act with

integrity in carrying out Licenced Function.

Jan 2022 Gilles Knowingly involved in the Unlawful Cash Service Fine of USD 175,000;

Rollet, for (authorised and facilitated Unlawful Cash Services, at Prohibited from holding office in or being

mer SEO, times through the use of his own bank account) an employee of a regulated DIFC entity.

La Tresorer Involvement in the use of false invoices and the transfer Restricted from performing any function

ie of client money to unregulated companies outside the in connection with the provision of

DIFC Financial Services in or from the DIFC.

Appealed to the FMT where DFSA’s decision was upheld

in Jan, 2022.

55.

55

• The DFSA expects all firms to implement an appropriate framework to identify and mitigate

cyber risks and to detect, respond to, and recover from cyber incidents.

• All members of senior management at both the board and executive levels need to be aware

of their firm’s cyber vulnerabilities, and accordingly, provide the necessary resources, control

and oversight to manage the risk

• DFSA published Cybersecurity Guidelines in order to assist Firms in:

o establishing a sound and robust cyber risk management framework; and

o strengthening system security, reliability, resiliency, and recoverability.

• EAL’s Cybersecurity Policy was finalised in Feb 2022. The objectives of this Policy are :

o To establish a sound and robust cyber risk management framework;

o To strengthen system security, reliability, resiliency, and recoverability; and

o To ensure cybersecurity risks are properly managed within the Firm.

56.

56

Cybersecurity (contd..)

Key components of the firm’s Cybersecurity Policy:

• Cybersecurity governance: Defining roles and responsibilities of:

o Board

o senior management

o Risk Officer

o employees;

o Third-party service providers.

• Cybersecurity incident response plan and team

• Defining Material Cyber Incidents and describing process to report the same

• Systems Access

o authorized use

o passwords

o third party access

o internet security;

• Cybersecurity controls

o access rights

o change management

o network security

o malware and phishing

o remote access

o lost devices